Research on Green Finance and Green Development Based Eco-Efficiency and Spatial Econometric Analysis

Abstract

:1. Introduction

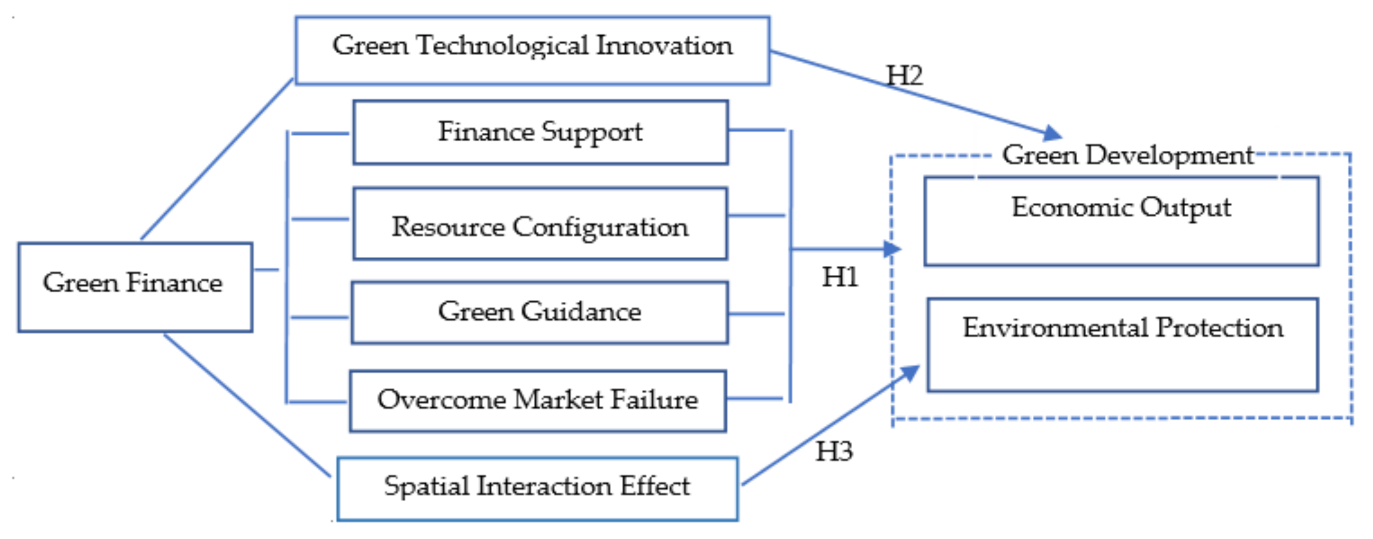

2. Theoretical Analysis and Research Hypotheses

3. Study Design

3.1. Measurement of Green Development

3.1.1. Super-Efficiency SBM Model

3.1.2. Super-Efficiency SBM Window Model

3.2. Measurement of Green Finance

3.3. Variables, Methodology and Data

3.3.1. Explanatory Variables

3.3.2. Spatial Panel Data Model

3.3.3. Samples and Data Sources

4. Empirical Results of the Models and Discussion

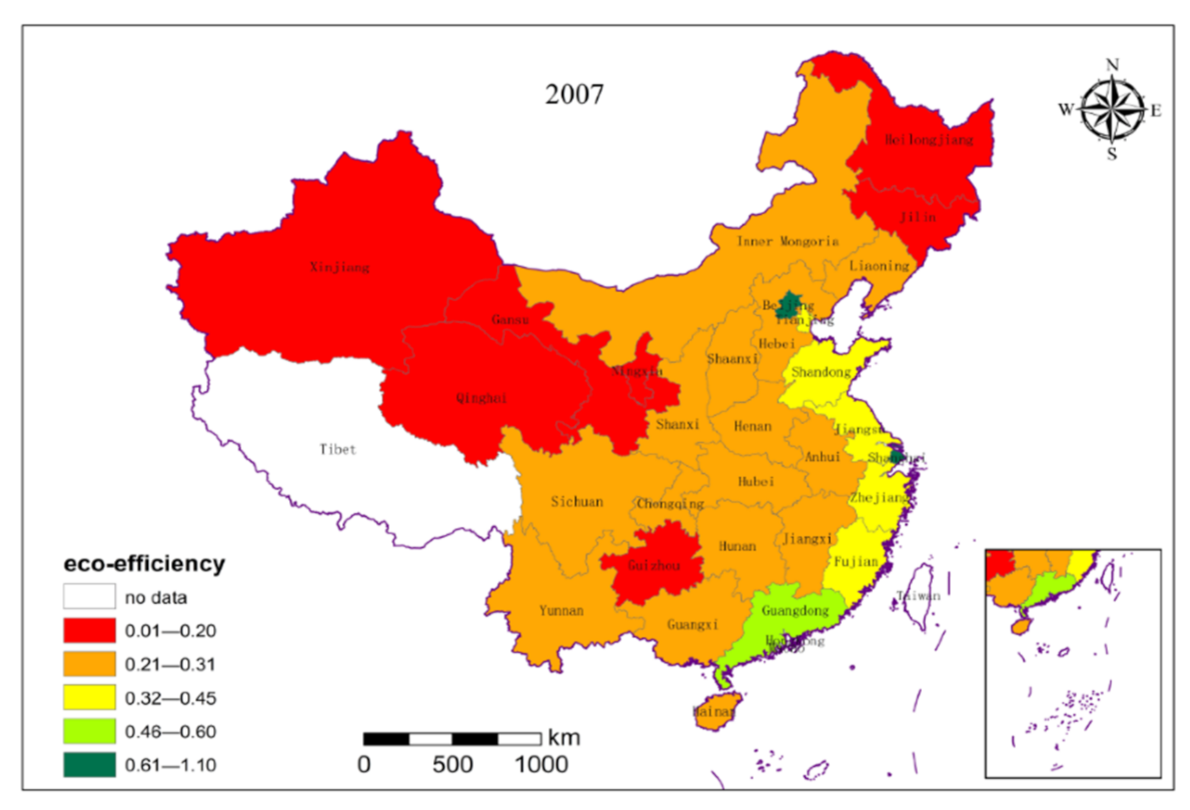

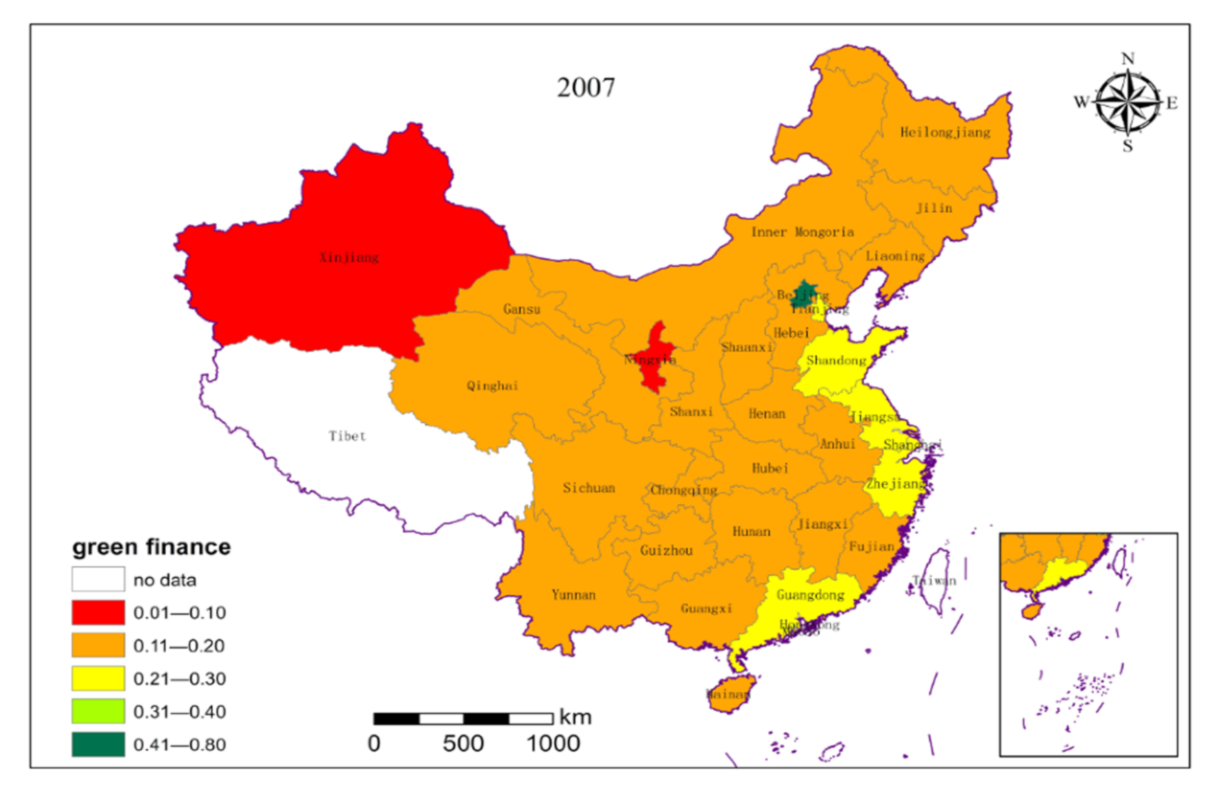

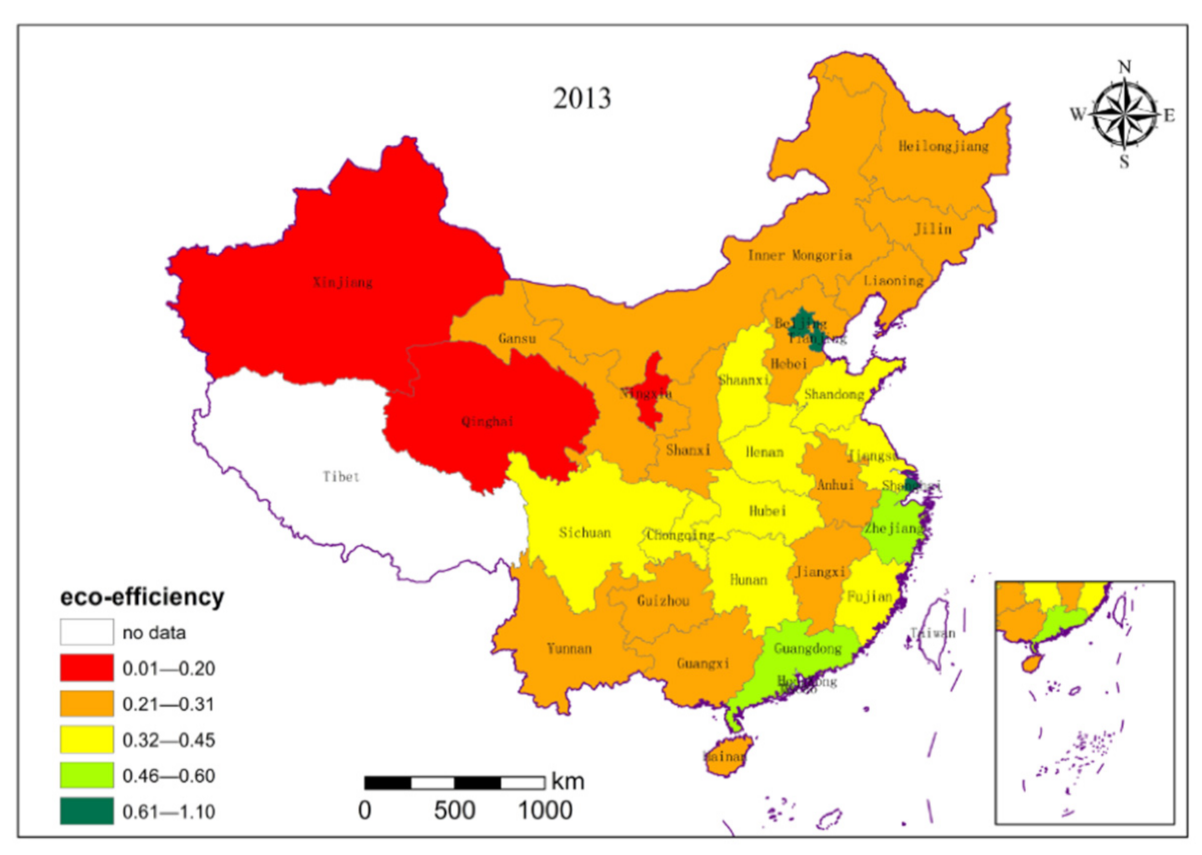

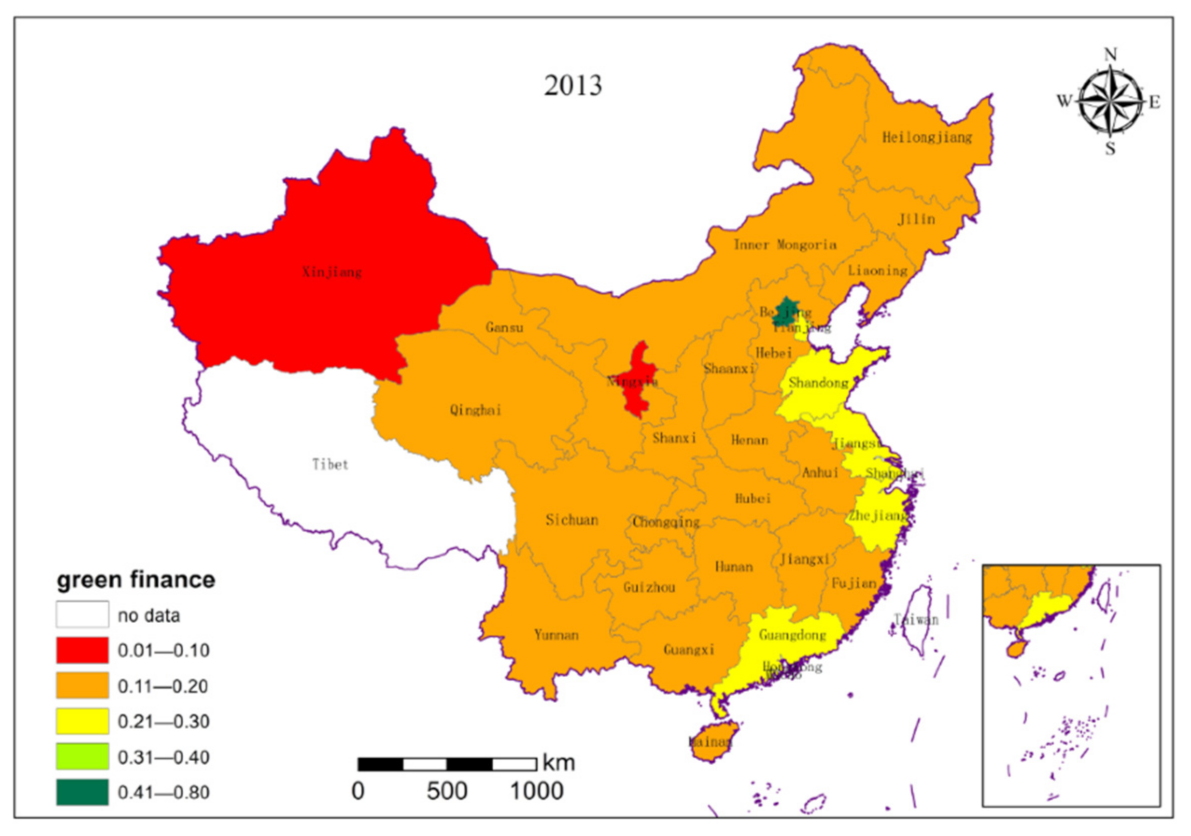

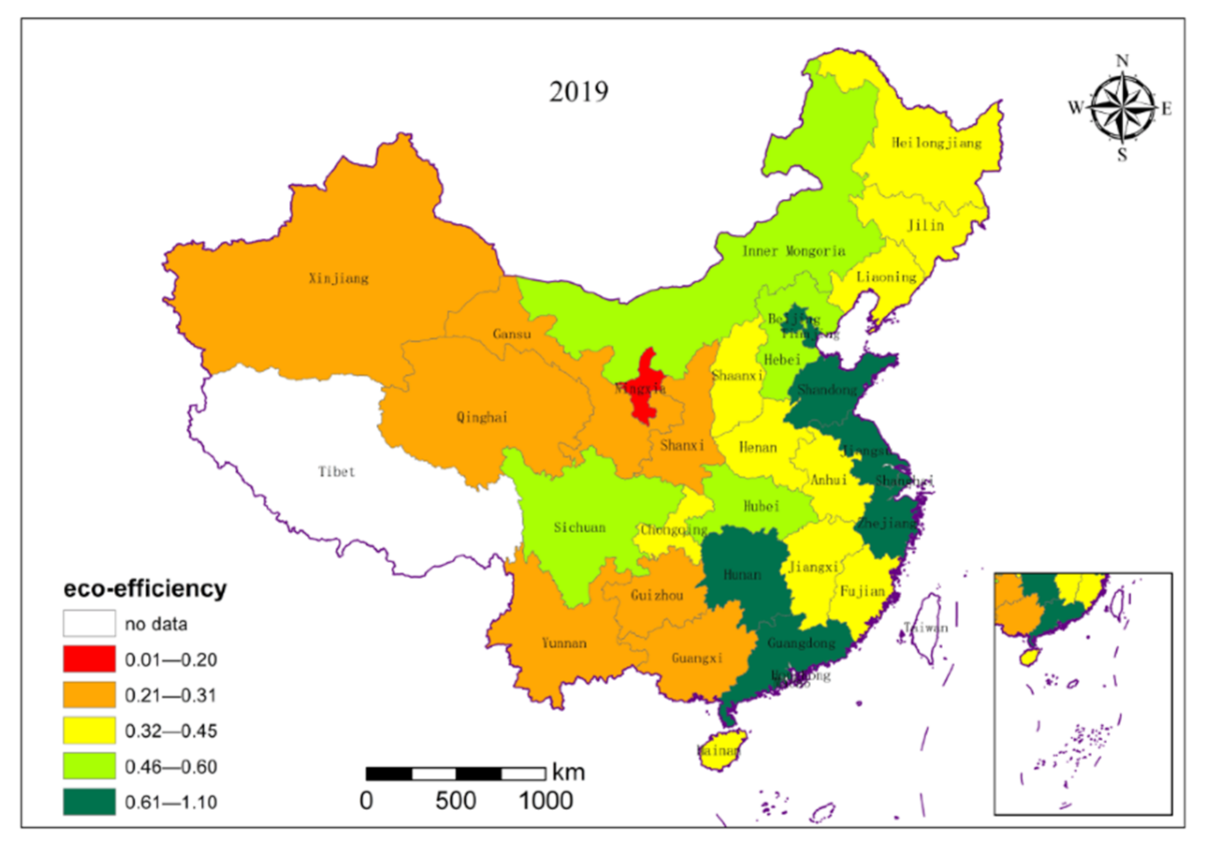

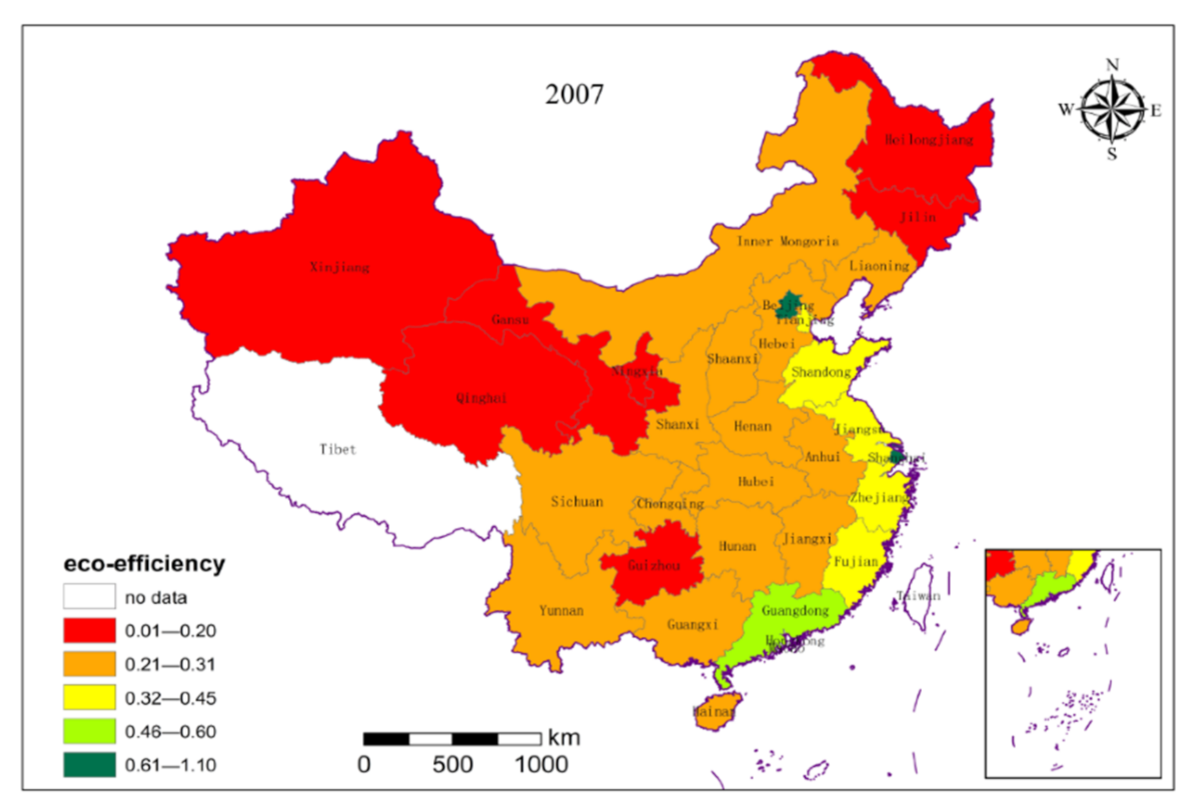

4.1. The Temporal and Spatial Changes and Connection of Regional Green Finance and Eco-Efficiency

4.2. Results and Discussion

4.2.1. Selection of Model and Estimation Methods

4.2.2. Nationwide

4.2.3. Eastern Region

4.2.4. Central Region

4.2.5. Western Region

5. Control for Endogeneity and Robustness Test

5.1. Control for Endogeneity

5.2. Robustness Test

5.2.1. Change the Measurement of the Dependent Variable

5.2.2. Change the Way the Spatial Weight Is Constructed

6. Conclusions and Further Research

6.1. Conclusions

6.2. Limitations and Further Research

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Acknowledgments

Conflicts of Interest

References

- Chami, R.; Cosimano, T.F.; Fullenkamp, C. Managing Ethical Risk: How Investing in Ethics Adds Value. J. Bank. Financ. 2002, 26, 1697–1781. [Google Scholar] [CrossRef]

- Jeucken, J. Sustainable Finance and Banking; The Earths Can Publication: Sterling, VA, USA, 2006. [Google Scholar]

- Scholtens, B. Finance as a Driver of Corporate Social Responsibility. J. Bus. Ethics 2006, 68, 19–33. [Google Scholar] [CrossRef]

- Graham, A.; Maher, J.J.; Northcut, W.D. Environmental Liability Information and Bond Ratings. J. Account. Audit. Financ. 2001, 16, 93–116. [Google Scholar] [CrossRef]

- Tang, A.; Chiara, N.; Taylor, J.E. Financing Renewable Energy Infrastructure: Formulation, Pricing and Impact of a Carbon Revenue Bond. Energy Policy 2012, 45, 691–703. [Google Scholar] [CrossRef]

- Ye, Y. The “Equator” Journey of “Green Credit”. Environ. Prot. 2008, 7, 46–48. (In Chinese) [Google Scholar] [CrossRef]

- Yang, Y.; Li, Y.X.L.; Shen, H.T. Green Financial Policies, Corporate Governance and Environmental Disclosure: A Case Study of 502 Listed Firms in Heavy Pollution Industry. Financ. Trade Res. 2011, 22, 131–139. (In Chinese) [Google Scholar]

- Hu, C.S.; Cai, J.S.; Ding, Y.; Ding, Y. Corporate Behavior Restructuring under the Path of Green Finance. Sci. Econ. Soc. 2013, 31, 48–51. (In Chinese) [Google Scholar]

- Salazar, J. Environmental Finance: Linking Two World. In Proceedings of the Workshop on Financial Innovations for Biodiversity, Bratislava, Slovakia, 1–3 May 1998; pp. 2–18. [Google Scholar]

- Anderson, J. Environmental Finance. In Handbook of Environmental and Sustainable Finance; Ramiah, V., Gregoriou, G.N., Eds.; Elsevier Inc.: Amsterdam, The Netherlands, 2016. [Google Scholar]

- Wang, E.; Liu, X.; Wu, J.; Cai, D. Green Credit, Debt Maturity, and Corporate Investment—Evidence from China. Sustainability 2019, 11, 583. [Google Scholar] [CrossRef] [Green Version]

- Chen, W.G.; Hu, D. An Analysis of the Functional Mechanism and Effect of Green Credit on Industrial Upgrading. J. Jiangxi Univ. Financ. Econ. 2011, 4, 12–20. (In Chinese) [Google Scholar]

- Cai, H.J. Research on the Influence of Green Credit on my country’s Industrial Transformation and Upgrading under the New Normal. Friends Account. 2015, 13, 16–19. (In Chinese) [Google Scholar]

- Long, Y.A.; Chen, G.Q. Green Finance Development and Industrial Structure Optimization under the Background of “Beautiful China”. Enterp. Econ. 2018, 37, 11–18. (In Chinese) [Google Scholar]

- Gao, J.J.; Zhang, W.W. Research on the Impact of Green Finance on the Ecologicalization of China’s Industrial Structure. Econ. Rev. J. 2021, 2, 105–115. (In Chinese) [Google Scholar]

- White, M.A. Environmental finance: Value and risk in an age of ecology. Bus. Strategy Environ. 1996, 5, 198–206. [Google Scholar] [CrossRef]

- Jeucken, M.; Bouma, J. The changing environment of banks. Greener Manag. Int. 1999, 27, 24–38. [Google Scholar] [CrossRef]

- Jeucken, M. Sustainable Finance and Banking; Earthscan Publications Ltd.: London, UK, 2001. [Google Scholar]

- Lioui, A.; Sharma, Z. Environmental corporate social responsibility and financial performance: Disentangling direct and indirect effects. Ecol. Econ. 2012, 78, 100–111. [Google Scholar] [CrossRef]

- Kim, Y.; Li, H.; Li, S. Corporate social responsibility and stock price crash risk. J. Bank. Financ. 2014, 43, 1–13. [Google Scholar] [CrossRef] [Green Version]

- Linnenluecke, M.K.; Smith, T.; Mcknight, B. Environmental finance: A research agenda for interdisciplinary finance research. Econ. Model. 2016, 59, 124–130. [Google Scholar] [CrossRef]

- Liu, X.L.; Wen, S.Y. Should financial institutions in China bear environmental responsibility? Basic facts, theoretical models and empirical tests. Econ. Res. 2019, 54, 38–54. (In Chinese) [Google Scholar]

- Research Group of Tianda Research Institute. China’s Green Financial System: Construction and Development Strategy. Financ. Trade Econ. 2011, 10, 38–46, 135. [Google Scholar]

- Green Finance Working Group. Building China’s Green Financial System; China Finance Press: Beijing, China, 2015; pp. 87–98. [Google Scholar]

- Wang, Y. Important Roles of Green Finance in Promoting Green Economic Recovery. Financ. Perspect. J. 2020, 10, 15–19. [Google Scholar]

- Hu, A.G. China’s Goal of Achieving Carbon Peak by 2030 and Its Main Approaches. J. Beijing Univ. Technol. Soc. Sci. Ed. 2021, 21, 1–15. (In Chinese) [Google Scholar]

- AN, G.J. Discussion on the Path of Green Finance Innovation under the Goal of Carbon Neutrality. South China Financ. 2021, 2, 87–96. (In Chinese) [Google Scholar]

- Ning, W.; She, J.H. An Empirical Study on the Dynamic Relationship between Green Finance and Macroeconomic Growth. Seeker 2014, 10, 62–66. (In Chinese) [Google Scholar]

- Falcone, P.M.; Sica, E. Assessing the Opportunities and Challenges of Green Finance in Italy: An Analysis of the Biomass Production Sector. Sustainability 2019, 11, 517. [Google Scholar] [CrossRef] [Green Version]

- Ionescu, L. Leveraging Green Finance for Low-Carbon Energy, Sustainable Economic Development, and Climate Change Mitigation during the COVID-19 Pandemic. Rev. Contemp. Philos. 2021, 20, 175–186. [Google Scholar]

- Wen, S.Y.; Lin, Z.F.; Liu, X.L. Green finance and economic growth quality: Construction and empirical testing of a general equilibrium model with resource and environmental constraints. Chin. J. Manag. Sci. 2021. (In Chinese) [Google Scholar] [CrossRef]

- Perroux, F. The Pole of Development’s New Place in a General Theory of Economic Activity; Regional Economic Development: Boston, MA, USA, 1988; pp. 1–29. [Google Scholar]

- Levine, R. Finance and growth: Theory, evidence and mechanisms. In Handbook of Economic Growth; North-Holland Press: North Holland, The Netherlands, 2005. [Google Scholar]

- Bai, Q.; Tan, Q. Analysis on evolution and development of financial function. J. Financ. Res. 2006, 7, 41–52. (In Chinese) [Google Scholar]

- Zhang, B.; Bi, J.; Fan, Z.; Yuan, Z.; Ge, J. Eco-efficiency analysis of industrial system in China: A data envelopment analysis approach. Ecol. Econ. 2008, 68, 306–316. [Google Scholar] [CrossRef]

- Picazo-Tadeo, A.J.; Beltrán-Esteve, M.; Gómez-Limón, J.A. Assessing eco-efficiency with directional distance functions. Eur. J. Oper. Res. 2012, 220, 798–809. [Google Scholar] [CrossRef]

- Huang, J.; Yang, X.; Cheng, G.; Wang, S. A comprehensive eco-efficiency model and dynamics of regional eco-efficiency in China. J. Clean. Prod. 2014, 67, 228–238. [Google Scholar] [CrossRef]

- Ye, T.; Zheng, H.; Ge, X.; Yang, K. Pathway of Green Development of Yangtze River Economics Belt from the Perspective of Green Technological Innovation and Environmental Regulation. Int. J. Environ. Res. Public Health 2021, 18, 10471. [Google Scholar] [CrossRef]

- Reinhard, S.; Knox, C.A.; Geert, L.; Thijssen, J. Environmental efficiency with multiple environmentally detrimental variables; estimated with SFA and DEA. Eur. J. Oper. Res. 2000, 121, 287–303. [Google Scholar] [CrossRef]

- Zhang, X.P.; Cheng, X.M.; Yuan, J.H.; Gao, X.J. Total-factor Energy Efficiency in Developing Countries. Energy Policy 2011, 39, 644–650. [Google Scholar] [CrossRef]

- Kasayanond, A.; Umam, R.; Jermsittiparsert, K. Environmental Sustainability and its Growth in Malaysia by Elaborating the Green Economy and Environmental Efficiency. Int. J. Energy Econ. Policy 2019, 9, 465–473. [Google Scholar] [CrossRef] [Green Version]

- Su, S.; Zhang, F. Modeling the role of environmental regulations in regional green economy efficiency of China: Empirical evidence from super efficiency DEA-Tobit model. J. Environ. Manag. 2020, 261, 110227. [Google Scholar]

- Charnes, A.; Cooper, W.W.; Rhodes, E. Measuring the efficiency of decision making units. Eur. J. Oper. Res. 1978, 2, 429–444. [Google Scholar] [CrossRef]

- Tone, K. A slacks-based measure of super-efficiency in data envelopment analysis. Eur. J. Oper. Res. 2002, 143, 32–41. [Google Scholar] [CrossRef] [Green Version]

- Tone, K. A slacks-based measure of efficiency in data envelopment analysis. Eur. J. Oper. Res. 2001, 130, 498–509. [Google Scholar] [CrossRef] [Green Version]

- Charnes, A.; Cooper, W.W. Programming with linear fractional functionals. Nav. Res. Logist. Q. 1962, 15, 333–334. [Google Scholar] [CrossRef]

- Charnes, A.; Cooper, W.W.; Lewin, A.Y.; Seiford, L.M. Extensions to DEA Models, Data Envelopment Analysis: Theory, Methodology, and Application; Kluwer Academic Publishers: Norwell, MA, USA, 1994. [Google Scholar]

- Li, X.; Xia, G. China Green Finance Report 2014; China Finance Press: Beijing, China, 2014; pp. 21–45. [Google Scholar]

- Costantini, V.; Crespi, F.; Palma, A. Characterizing the policy mix and its impact on eco-innovation: A patent analysis of energy-efficient technologies. Res. Pol. 2017, 46, 799–819. [Google Scholar] [CrossRef]

- He, X.G.; Zhang, Y.H. Factors influencing industrial carbon emissions and CKC restructuring effect in China: An empirical study of dynamic panel data by industry based on STIRPAT model. China Ind. Econ. 2012, 1, 26–35. (In Chinese) [Google Scholar]

- Yu, Z.X.; Chen, J.D.; Jie, M. The road to low carbon economy: A perspective of industrial planning. Econ. Res 2020, 55, 116–132. (In Chinese) [Google Scholar]

- Ma, L.M.; Zhang, X. The Spatial Effect of China’s Haze Pollution and the Impact from Economic Change and Energy Structure. Chin. Ind. Econ. 2014, 4, 19–31. [Google Scholar]

- Jorgenson, A.K.; Dick, C. Foreign Direct Investment, Environmental INGO Presence and Carbon Dioxide Emissions in Less-Developed Countries, 1980–2000. Rev. Int. Organ. 2010, 4, 129–146. [Google Scholar]

- Ge, X.; Zhou, Z.; Zhou, Y.; Ye, X.; Liu, S. A Spatial Panel Data Analysis of Economic Growth, Urbanization, and NOx Emissions in China. Int. J. Environ. Res. Public Health 2018, 15, 725. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Elhorst, J.P. Spatial Econometrics: From Cross-Sectional Data to Spatial Panels; Springer: Berlin/Heidelberg, Germany, 2014; pp. 37–67. [Google Scholar]

- LeSage, J.; Pace, R.K. Introduction to Spatial Econometrics; Chapman & Hall/CRC: Boca Raton, FL, USA, 2009. [Google Scholar]

- Elhorst, J.P. Applied spatial econometrics: Raising the bar. Spat. Econ. Anal. 2010, 5, 9–28. [Google Scholar] [CrossRef]

- Elhorst, J.P.; Fréret, S. Evidence of political yardstick competition in France using a two-regime spatial Durbin model with fixed effect. J. Reg. Sci. 2009, 49, 931–951. [Google Scholar] [CrossRef]

- Lin, M.J.; Liu, J.T. Do lower birth weight babies have lower grades? Twin fixed effect and instrumental variable method evidence from Taiwan. Soc. Sci. Med. 2009, 68, 1780–1787. [Google Scholar] [CrossRef]

- Chong, W.L. Measuring trade creating effects of RTAs: A fixed effect estimation approach. East Asian Econ. Rev. 2017, 12, 139–155. [Google Scholar] [CrossRef]

- Liu, Y.Q.; Zhu, J.L.; Li, E.Y.; Meng, Z.Y.; Song, Y. Environmental regulation, green technological innovation, and eco-efficiency: The case of Yangtze river economic belt in China. Technol. Forecast. Soc. Chang. 2020, 155, 119993. [Google Scholar] [CrossRef]

- Bianchini, R.; Croce, A. The Role of Environmental Policies in Promoting Venture Capital Investments in Cleantech Companies. Rev. Corp. Financ. 2022, 2, in press. [Google Scholar]

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

| Windows | … | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | |||||||||||

| 2 | |||||||||||

| 3 | |||||||||||

| … | … | ||||||||||

| Average value |

| Tier 1 Indicators | Secondary Indicators | Tertiary Indicators (Unit) |

|---|---|---|

| Input | Capital investment | Investment in Fixed Assets (CNY 10,000) |

| Resource input | Energy Consumption (10,000 tce) | |

| Water Supply (10,000 tons) | ||

| Area of Land Used for Urban Construction (square kilometer) Cultivated Area (square kilometer) | ||

| Employment (10,000 people) | ||

| Desirable output | Regional development indicators | Regional Gross Domestic Product (CNY 10,000) |

| Undesirable output | Environmental benefit indicators | Volume of Industrial Wastewater Discharged (10,000 tons) |

| Volume of Sulphur Dioxide Emission (ton) | ||

| Volume of Industrial Dust Emission (ton) |

| First Level Indicators | Secondary Indicators | Definition |

|---|---|---|

| Green credit | Proportion of interest expenditure of high-energy-consumption industries | Interest expenditures of the six high- energy- consuming industries/total interest expenditures of industrial industries |

| Green securities | Market value of environmental protection enterprises | Market value of environmental protection enterprises /total market value of A shares |

| Market value of high-energy- consuming industries | Market value of the six high-energy-consuming industries/total market value of A shares | |

| Green insurance | Proportion of agricultural insurance scale | Agricultural insurance expenditure/total insurance expenditure |

| Compensation rate of agricultural insurance | Agricultural insurance expenditure/agricultural insurance income | |

| Green investment | Proportion of energy-saving and environmental protection expenditure | Energy-saving and environmental protection industry fiscal expenditure/total fiscal expenditure |

| Percentage of investment in environmental pollution control | Investment in pollution control /GDP |

| Variables | Moran’I | p-Value | Geary’s c | p-Value |

|---|---|---|---|---|

| EE | 0.227 | 0.009 | 0.570 | 0.003 |

| GF | 0.146 | 0.023 | 0.460 | 0.029 |

| Variable | Whole Country | East Region | Central Region | West Region |

|---|---|---|---|---|

| W × EE | 0.1486 ** (2.03) | 0.1531 * (1.82) | −0.3776 ***(−3.50) | −0.3863 ***(−3.18) |

| gf | 0.3015 * (1.80) | 0.2240 ** (2.22) | 1.8536 (1.36) | −0.6275 * (−1.88) |

| gf × ln (gti + 1) | 0.0722 ** (2.30) | 0.1622 ** (2.57) | −0.0881 (−0.41) | −0.1291 * (1.82) |

| ln (gti + 1) | −0.0072 (−0.86) | 0.0629 *** (3.20) | −0.0096 (−0.33) | −0.0201 * (−1.68) |

| open | 0.0015 (0.15) | 0.0086 (0.66) | 0.3463 *** (5.29) | −0.0037 (−0.09) |

| urb | 0.3553 *** (3.46) | 0.3922 ** (2.18) | −0.2478 (−1.20) | −0.9677 ***(−3.30) |

| es | −0.0435 ***(−2.71) | 0.3238 *** (2.99) | 0.1196 ** (2.10) | −0.0248 (−1.56) |

| lnpgdp | 0.1803 *** (6.83) | 0.2176 *** (3.22) | 0.3490 *** (5.38) | 0.3053 *** (8.66) |

| W × gf | −2.8247 ***(−5.39) | 2.1068 (1.11) | 1.9274 (1.09) | −0.8361 * (−1.77) |

| W × gf × ln (gti + 1) | −0.2078 ***(−2.62) | 0.2168 (1.49) | −0.4642 * (−1.66) | −0.2174 * (1.72) |

| W × lngti | 0.0223 (1.09) | 0.0714 ** (2.05) | 0.0731 * (1.70) | −0.0163 (−0.86) |

| W × open | 0.0910 *** (4.16) | −0.0590 * (−1.90) | −0.0432 (−0.32) | 0.1019 (1.55) |

| W × urb | −0.0452 (−0.27) | 0.6740 ** (2.36) | 0.1537 (0.26) | −1.8368 ***(−4.19) |

| W × es | −0.0028 (−0.09) | 0.7092 *** (3.85) | −0.0918 (−1.44) | −0.0589 ** (−2.08) |

| W × lnpgdp | 0.1816 *** (3.44) | −0.1921 (−1.62) | 0.5633 *** (4.38) | 0.1753 ** (2.46) |

| R2 | 0.6827 | 0.8467 | 0.2041 | 0.5095 |

| LogL | 459.4799 | 177.2615 | 237.3615 | 331.9666 |

| 0.0055 *** | 0.0049 *** | 0.0005 *** | 0.0005 *** | |

| LM-test | 29.391 *** | 7.444 *** | 8.625 *** | 11.111 *** |

| LR_spatial_lag | 31.12 *** | 27.05 *** | 53.31 *** | 41.53 *** |

| LR_spatial_err | 37.88 *** | 27.10 *** | 34.82 *** | 16.32 *** |

| Hausman-test | 37.50 *** | 35.33 *** | 36.11 *** | 34.29 *** |

| Variable | Nationwide | Eastern Region | Central Region | Western Region | |

|---|---|---|---|---|---|

| Direct Effect | gf | 0.2044 (1.13) | 0.3908 ** (2.12) | 1.6379 (1.13) | −0.5457 * (−1.78) |

| gf × ln (gti + 1) | 0.0793 (1.02) | 0.1461 ** (2.12) | 0.0009 (0.00) | −0.2111 ** (−2.32) | |

| ln (gti + 1) | −0.0065 (−0.78) | 0.0584 *** (2.85) | −0.0275 (−0.89) | −0.0195 ** (−2.21) | |

| Open | 0.0058 (0.62) | 0.0060 (0.46) | 0.3926 *** (5.45) | −0.0095 *** (−3.22) | |

| Urb | 0.3491 *** (3.49) | 0.4401 ** (2.49) | −0.3109 (−1.21) | −0.8347 *** (−2.69) | |

| es | −0.0433 *** (−2.73) | −0.3872 *** (−3.36) | 0.1515 *** (2.75) | −0.0202 (−1.34) | |

| lnpgdp | 0.1896 *** (7.35) | 0.2113 *** (2.95) | 0.2590 *** (4.12) | 0.3018 *** (7.92) | |

| Indirect Effect | gf | −3.2098 *** (−5.02) | 0.1789 *** (3.07) | 1.1209 (0.72) | −0.3184 ** (−2.35) |

| gf × ln (gti + 1) | −0.2537 *** (−2.88) | 0.1120 ** (2.25) | −0.3979 (−1.66) | −0.1391 * (−1.79) | |

| ln (gti + 1) | 0.0243 (1.07) | 0.0696 * (1.81) | 0.0747 (1.01) | −0.0065 (−0.37) | |

| open | 0.1052 (1.14) | −0.0626 * (−1.77) | −0.1608 (−1.26) | 0.0832 (1.44) | |

| urb | 0.0105 (0.05) | 0.3063 ** (2.56) | 0.2389 (0.43) | −0.2026 (−1.07) | |

| es | −0.0104 (−0.26) | −0.8632 (−1.04) | −0.1248 ** (−2.04) | −0.0386 * (−1.66) | |

| lnpgdp | 0.2381 (1.17) | 0.1666 ** (2.17) | 0.1070 *** (3.39) | 0.0462 (0.85) | |

| Total Effect | gf | −3.0054 ** (−2.28) | 0.5697 ** (2.48) | 2.7588 (1.53) | −0.8641 * (−1.75) |

| gf × ln (gti + 1) | −0.1744 ** (−2.13) | 0.2581 ** (2.29) | −0.3971 (−1.37) | −0.3502 * (−1.72) | |

| ln (gti + 1) | 0.0178 (0.70) | 0.0112 (0.22) | 0.0473 (1.20) | −0.0260 ** (−2.50) | |

| open | 0.1110 (0.98) | −0.0566 (−1.39) | 0.2317 ** (2.06) | 0.0737 (1.54) | |

| urb | 0.3596 ** (2.21) | 0.7464 ** (2.22) | −0.0720 (−0.15) | −1.0373 ** (−2.23) | |

| es | −0.0536 * (−1.92) | −1.2504 * (−1.88) | 0.0266 (0.35) | −0.0588 ** (−2.21) | |

| lnpgdp | 0.4277 ** (2.36) | 0.3779 ** (2.22) | 0.3660 *** (5.17) | 0.3480 *** (7.52) |

| Variable | Nationwide | Eastern Region | Central Region | Western Region | |

|---|---|---|---|---|---|

| Direct Effect | EE | −0.0431 (0.87) | 0.0403 (0.26) | 0.0156 (0.97) | −0.0228 (−1.48) |

| gf × ln (gti + 1) | 0.1301 *** (5.52) | 0.1202 *** (8.43) | 0.1491 *** (9.13) | 0.0976 *** (9.31) | |

| ln (gti + 1) | −0.0304 (1.43) | −0.0329 (−1.52) | −0.0169 (−0.34) | −0.0129 (−0.22) | |

| open | 0.0009 (0.75) | −0.0026 (−1.61) | −0.0108 ** (−2.16) | −0.0011 (−0.19) | |

| urb | 0.1197 *** (4.49) | 0.1206 ** (2.11) | 0.0267 (1.59) | −0.0698 (−1.60) | |

| es | −0.0104 ** (−2.53) | −0.1215 *** (−4.85) | −0.0001 (−0.03) | −0.0043 * (−1.84) | |

| lnpgdp | 0.0029 ** (2.42) | 0.0042 *** (3.21) | 0.0031 (0.52) | 0.0059 (0.94) | |

| Indirect Effect | EE | −0.0698 (−1.06) | 0.0278 (1.01) | 0.0450 (0.26) | −0.0735 (−0.92) |

| gf × ln (gti + 1) | 0.0070 (1.21) | −0.0151 ** (−2.28) | 0.0271 (3.68) | −0.0776 *** (−5.67) | |

| ln (gti + 1) | 0.0005 (0.20) | 0.0092 (0.97) | −0.0017 (−0.94) | 0.0108 (3.52) | |

| open | −0.0010 (−0.39) | 0.0030 (0.79) | −0.0096 (−1.03) | 0.0046 (0.30) | |

| urb | 0.2512 ** (2.29) | 0.4507 ** (2.10) | 0.0462 (1.13) | 0.0832 (0.95) | |

| es | 0.0139 * (1.83) | 0.0645 * (1.86) | 0.0023 (0.48) | −0.0010 (−0.20) | |

| lnpgdp | 0.0053 (0.60) | 0.0013 (0.09) | −0.0451 (−0.53) | 0.0211 (1.48) | |

| Total Effect | EE | −0.1129 (−0.93) | 0.0125 (0.67) | 0.0606 (0.90) | −0.0963 (−0.42) |

| gf × ln (gti + 1) | 0.1371 *** (4.46) | 0.1051 *** (4.02) | 0.1761 (7.61) | 0.0200 (1.25) | |

| ln (gti + 1) | −0.0299 (1.04) | −0.0329 (−1.01) | −0.0186 * (−1.82) | −0.0021 (−0.64) | |

| open | −0.0000 (−0.01) | 0.0004 (0.11) | −0.0204 ** (−2.00) | 0.0035 (0.21) | |

| urb | 0.3708 *** (4.95) | 0.5712 ** (2.23) | 0.0729 (1.64) | 0.0134 (0.13) | |

| es | 0.0035 (0.42) | −0.0571 (−1.43) | 0.0022 (0.28) | −0.0053 (−0.82) | |

| lnpgdp | 0.0082 ** (2.13) | 0.0055 ** (2.17) | −0.0420 (−0.12) | 0.0271 (1.57) |

| Variable | Nationwide | Eastern Region | Central Region | Western Region | |

|---|---|---|---|---|---|

| Direct Effect | gf | 1.1168 (1.40) | 0.3888 ** (2.63) | 6.4147 (0.47) | −11.6059 *** (−9.02) |

| gf × ln (gti + 1) | 0.1635 (1.57) | 0.1688 ** (2.20) | −1.6805 *** (−4.64) | −2.8523 *** (−5.95) | |

| ln (gti + 1) | 0.0725 (1.43) | 0.0309 ** (2.21) | −0.2194 *** (4.01) | −0.4783 *** (−4.28) | |

| open | −0.0924 *** (−4.34) | −0.0767 *** (−5.53) | −0.4253 *** (−2.99) | −0.3018 (−0.63) | |

| urb | 0.4751 (1.04) | 0.1113 (0.29) | 1.6042 *** (3.53) | 9.7687 *** (6.92) | |

| es | −1.0090 *** (−13.78) | −0.1987 (−0.81) | −0.6372 *** (−5.76) | −0.5000 *** (−4.22) | |

| lnpgdp | 1.0236 *** (8.90) | 0.6025 *** (4.97) | 0.7042 *** (6.30) | 1.8106 *** (6.52) | |

| Indirect Effect | gf | −0.8546 ** (−2.41) | 0.1224 * (1.69) | 3.4151 (1.04) | −5.2027 *** (−2.75) |

| gf × ln (gti + 1) | −0.0909 * (−1.92) | 0.0540 ** (2.11) | −0.6042 (−1.39) | −1.5727 *** (−3.11) | |

| ln (gti + 1) | −0.0130 (−0.33) | 0.0098 * (1.91) | −0.0794 (−1.28) | 0.2590 (1.39) | |

| open | 0.0197 (0.41) | 0.0252 *** (3.35) | 0.5640 ** (2.26) | 1.1550 (1.46) | |

| urb | 3.3415 *** (4.91) | −0.0356 (−0.28) | 0.5441 (0.44) | −8.5091 *** (−4.24) | |

| es | 0.3383 ** (2.27) | 0.0654 (0.79) | 0.0618 (0.48) | −0.6394 *** (−2.99) | |

| lnpgdp | −0.3128 ** (−2.31) | 0.1977 *** (3.28) | −0.2599 (−1.26) | −1.5486 *** (−3.60) | |

| Total Effect | gf | 0.2622 (1.25) | 0.5112 * (1.93) | 9.8298 (1.43) | −16.8086 *** (−3.41) |

| gf × ln (gti + 1) | −0.0726 (−1.46) | 0.2228 ** (2.10) | −2.2847 ** (−2.50) | −4.4250 *** (0.30) | |

| ln (gti + 1) | 0.0594 (1.52) | 0.0407 * (1.90) | −0.2988 *** (−2.77) | −0.2193 (−1.40) | |

| open | −0.0727 (−1.46) | −0.0515 *** (−5.38) | 0.1387 (0.56) | 0.8533 (1.03) | |

| urb | 3.8165 *** (4.61) | 0.0758 (0.29) | 2.1483 * (1.68) | 1.2596 (0.50) | |

| es | −0.6707 *** (−3.98) | −0.1333 (−0.81) | −0.5754 *** (−3.18) | −1.1394 *** (−4.89) | |

| lnpgdp | 0.7108 *** (9.06) | 0.8002 *** (4.84) | 0.4443 *** (4.38) | 0.2620 ** (2.29) |

| Variable | Nationwide | Eastern Region | Central Region | Western Region | |

|---|---|---|---|---|---|

| Direct Effect | gf | 0.4570 (11.15) | 1.2304 *** (2.68) | 0.1311 (0.10) | −1.4923 *** (−2.62) |

| gf × ln (gti + 1) | 0.0708 (0.95) | 0.1367 * (1.90) | 0.1503 (0.75) | −0.2102 *** (−3.30) | |

| ln (gti + 1) | −0.0146 (−1.59) | 0.0629 *** (3.09) | −0.0484 * (−1.68) | −0.0331 *** (−2.88) | |

| open | 0.0117 (1.14) | −0.0579 *** (−3.52) | 0.3249 *** (4.69) | −0.0306 (−0.68) | |

| urb | 0.0475 (0.47) | 1.5297 *** (6.10) | −0.2534 (−1.07) | −1.6272 *** (−5.01) | |

| es | −0.0681 *** (−3.88) | −0.7571 *** (−5.20) | 0.0764 (1.50) | 0.0807 ** (2.27) | |

| lnpgdp | 0.2462 *** (8.72) | 0.1645 * (1.66) | 0.2977 *** (3.40) | 0.2568 *** (6.25) | |

| Indirect Effect | gf | −1.8850 (−1.43) | 0.9980 ** (2.38) | −1.1281 (−0.76) | −0.0548 ** (−2.36) |

| gf × ln (gti + 1) | −0.1646 ** (2.16) | 0.1523 ** (2.18) | 0.1315 (0.59) | −0.0347 ** (−2.33) | |

| ln (gti + 1) | 0.0485 (0.86) | 0.0570 (0.83) | 0.0170 (0.55) | 0.0146 (0.90) | |

| open | 0.1907 *** (2.93) | −0.4122 *** (−4.36) | −0.0918 (−0.89) | 0.1203 (1.01) | |

| urb | −0.1842 (−0.29) | 0.6980 *** (4.90) | −2.2384 *** (−4.65) | 0.7249 (1.18) | |

| es | −0.0683 (−0.59) | 2.8809 (0.76) | −0.1848 *** (−2.64) | −0.0432 ** (−2.24) | |

| lnpgdp | 0.2097 (0.90) | 0.0726 *** (3.53) | 0.1040 ** (2.57) | −0.0094 (−0.13) | |

| Total Effect | gf | −1.4280 (−1.02) | 2.2284 *** (2.63) | −0.9970 (−1.09) | −1.5471 *** (−2.93) |

| gf × ln (gti + 1) | −0.0938 (1.05) | 0.2890 ** (2.15) | 0.2818 (1.06) | −0.2449 *** (2.82) | |

| ln (gti + 1) | 0.0339 (0.57) | 0.1199 (0.07) | −0.0313 ** (−2.45) | −0.0184 (−1.50) | |

| open | 0.2025 *** (3.04) | −0.4701 *** (−4.40) | 0.2331 *** (3.23) | 0.0897 (1.19) | |

| urb | −0.1367 (−0.21) | 2.2277 *** (4.10) | −2.4918 *** (−5.73) | −0.9023 ** (−2.02) | |

| es | −0.1363 (−1.14) | 2.1238 (1.19) | −0.1084 (−1.63) | 0.0375 * (1.89) | |

| lnpgdp | 0.4559 * (1.89) | 0.2371 ** (2.27) | 0.4017 *** (6.73) | 0.2474 *** (3.57) |

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2022 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (https://creativecommons.org/licenses/by/4.0/).

Share and Cite

Ye, T.; Xiang, X.; Ge, X.; Yang, K. Research on Green Finance and Green Development Based Eco-Efficiency and Spatial Econometric Analysis. Sustainability 2022, 14, 2825. https://doi.org/10.3390/su14052825

Ye T, Xiang X, Ge X, Yang K. Research on Green Finance and Green Development Based Eco-Efficiency and Spatial Econometric Analysis. Sustainability. 2022; 14(5):2825. https://doi.org/10.3390/su14052825

Chicago/Turabian StyleYe, Tifang, Xiuli Xiang, Xiangyu Ge, and Keling Yang. 2022. "Research on Green Finance and Green Development Based Eco-Efficiency and Spatial Econometric Analysis" Sustainability 14, no. 5: 2825. https://doi.org/10.3390/su14052825

APA StyleYe, T., Xiang, X., Ge, X., & Yang, K. (2022). Research on Green Finance and Green Development Based Eco-Efficiency and Spatial Econometric Analysis. Sustainability, 14(5), 2825. https://doi.org/10.3390/su14052825